The quantum computing space is awash in buzz. Exciting technical breakthroughs and large financial investments have moved the conversation from technical publications to mainstream media and have prompted businesses to start considering their quantum strategies.

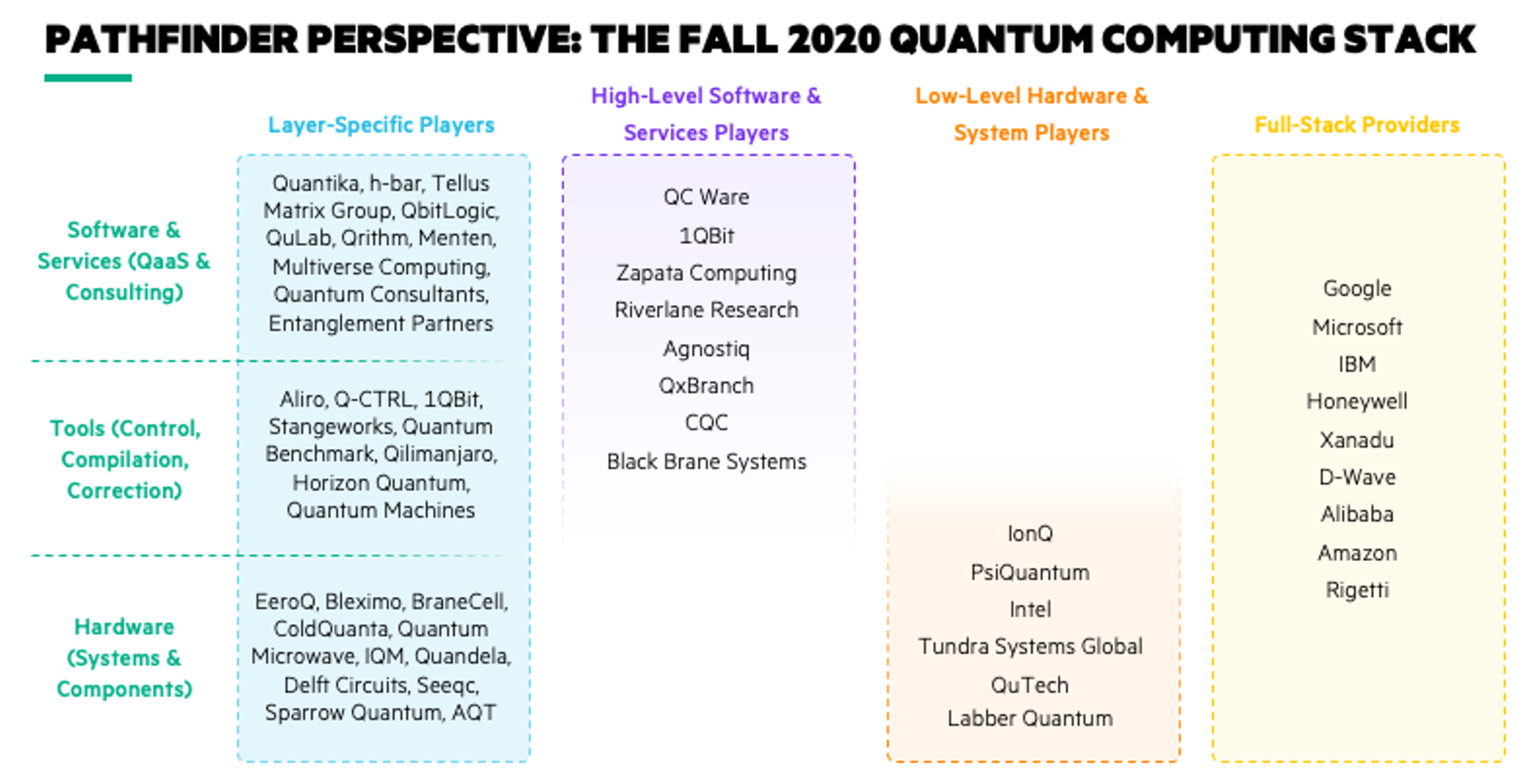

The quantum stack is still developing, but boundaries have emerged that make it possible to cluster new startups and incumbent players based on their technology. You can broadly segment the quantum computing stack into four layers: software and services, hardware, tools, and the complete solution (see table below).

We note most startups anchor themselves to one specific layer. This makes sense given the enormous technical, scientific, and engineering challenges many of these early-stage companies are solving. Interestingly, many of those challenges are within the hardware layer, where the rate of innovation — and investment — has been highest.

Another evident trend is hyperscale vendors (AWS, GCP, Azure) focusing on delivery of an end-to-end quantum computing solution via their cloud platforms. It should come as no surprise that these technology giants want to present quantum computing as another type of cloud resource, similar to CPUs and GPUs.

We see opportunity for additional innovation in the services, software, and tools layers. While the hardware players duke it out over whose qubits are better (trapped ion, neutral atoms, superconducting, topological, silicon spin, photonics), startups in these layers are working to identify algorithms and compilers that are best suited for individual applications.

Pathfinder looks forward to closely following the technical advancements and evolution of the startup ecosystem in the years to come.